The U.S. may be only a matter of weeks from defaulting on its debt, an unprecedented scenario that government officials have variously described as “unthinkable” and “catastrophic.”

With Republicans and Democrats remaining at an impasse for now, economists are examining the potential economic fallout if the situation comes to a head and the U.S. fails to make some payments.

In the event of a full-fledged debt default, the impact would be felt by anyone expecting funds from the government, whether a Social Security check, SNAP payment or government bond payout. But the impact wouldn’t be felt equally across the nation, Moody’s Analytics chief economist Mark Zandi said in a report this week.

“Most state economies will be hit hard if there is a debt limit breach, although the economic pain varies,” he and coauthors Adam Kamins and Bernard Yaros wrote.

Washington, D.C., where 1 in 4 jobs are tied to the federal government, would be hardest hit, becoming the “poster child” for a financial disaster, they said. States with large federal facilities, such as national laboratories or military bases, would be next in line. That includes Hawaii, which is home to the United States Pacific Command and to 11 military bases; Alaska, with vast federal land holdings; and New Mexico, home to Los Alamos National Laboratory.

“While the public sector typically serves as a stabilizing force, in the case of a breach it supercharges its economic fallout,” according to Moody’s.

Also vulnerable are regions that rely heavily on federal spending, including those with defense contractors. “Professional services firms suffer, hurting white-collar support firms in and around the Beltway, particularly Northern Virginia,” Moody’s said. “Aerospace is also hurt, impacting states including Connecticut, Kansas and Washington.”

Even a short debt ceiling breach, in which the government defaults for less than a week before lawmakers raise the government’s borrowing limit, would likely push the economy into a recession, according to Moody’s. In this scenario, 1.5 million people would lose their jobs, pushing unemployment from its current rate of 3.4% to 5%, while nation’s gross domestic product would shrink by 0.7%.

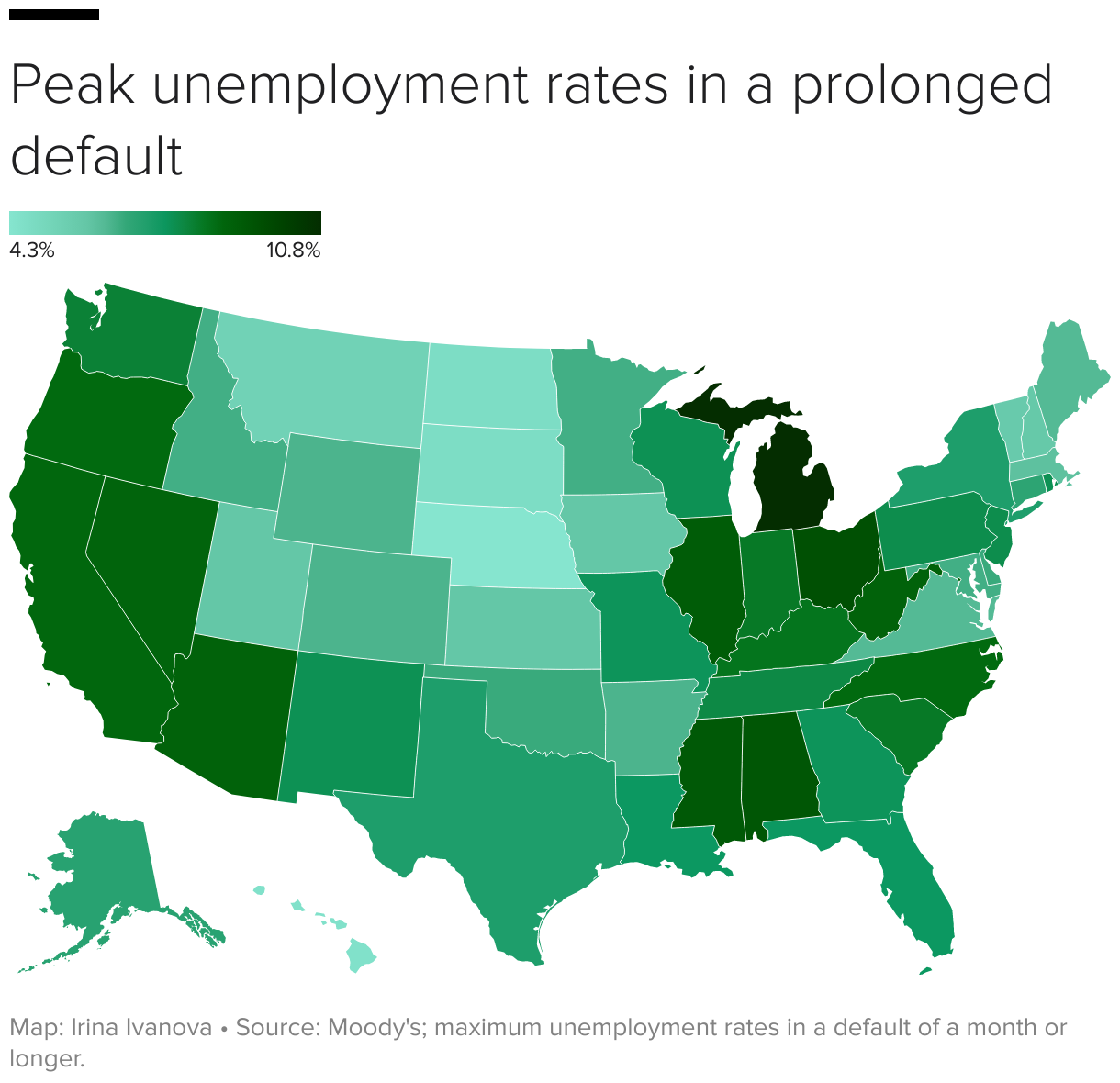

Moody’s also assesses the potential damage from a default lasting several months, an outcome it calls “cataclysmic.” The federal government would have no option but to slash its spending by about $150 billion. “As these cuts work through the economy, the hit to growth would be overwhelming,” Moody’s said.

“The economic downturn that would ensue would be comparable to that suffered during the global financial crisis,” with nearly 8 million jobs lost and the unemployment rate rising to 8%, according to the financial research firm. In this scenario, several states would suffer disproportionately, with Moody’s estimating that unemployment would top 9% in Alabama, Illinois, Ohio and Mississippi, while shooting up to nearly 11% in Michigan.

The turmoil would also likely depress stock prices by nearly 20%, vaporizing $10 trillion in household wealth held in 401(k) plans, pension funds and brokerage accounts, according to Moody’s. The cost of borrowing for households and businesses would soar.

Because of the enormous economic fallout of a debt default, it’s worth noting that Moody’s considers such an outcome highly unlikely. And if there is a breach, it’s likely to be short.

“But even a lengthy standoff no longer has a zero probability,” the analysts said. “What once seemed unimaginable now seems a real threat.”

{kind=link}